Interviewer’s Note: This column about fiduciary issues affecting public pension systems is the general responsibility of Suzanne Dugan, who usually writes the column or invites guests to offer some helpful commentary. Suzanne is the founder and head of the firm’s Ethics and Fiduciary Counseling practice, one of the country’s most active and recognized practices providing trusted counsel to public pension trustees and staff. Suzanne was recently named President of the National Association of Public Pension Attorneys (NAPPA). NAPPA is almost 40 years old and provides an important opportunity for public pension lawyers to come together to learn about the most critical matters affecting their work.

As Suzanne begins her one-year term as president of National Association of Public Pension Attorneys (NAPPA), she thought this a good moment to flip the seats so she can share a little bit about her work on your behalf and as the leader of this group. Since she and I have spent the last couple of decades working on and discussing public pensions, I’ll serve as the foil in this conversation. Hope you enjoy.

Luke Bierman: You’ve been chosen by your peers to lead NAPPA. Tell us a bit about the organization—how you became involved, how it’s organized, and how NAPPA is different from other organizations that work with public pensions.

Suzanne M. Dugan: NAPPA is the only national professional association focused exclusively on public pension attorneys. The beauty of the organization is that it provides an opportunity to exchange information, advance knowledge and education, and foster best principles and sound practices in the field of public employee retirement systems. Public pension plans are a bit unique as they are not governed by ERISA but rather by provisions enacted in their home jurisdictions. These laws might be similar across states and municipalities, allowing members to share their experiences very neatly, but can also vary across the country, giving legal practitioners opportunities to learn about these differences and apply those lessons by analogy. NAPPA’s singular focus on public pensions and its approach of similarity and difference separates it from other organizations.

The organization hosts two educational programs each year. The Winter Seminar devotes a half-day each to NAPPA’s four sections—Benefits, Fiduciary and Plan Governance (my personal favorite), Investments, and Tax—as well as general interest topics on the final morning of the program. The Legal Education Conference, which runs for four days, focuses more about the law and legal issues affecting public pension plans on a wide range of topics and provides public pension attorneys with an opportunity to obtain continuing legal education credit. It is not unusual for several hundred lawyers to attend these programs, which are organized by the four sections I mentioned, as well as our education committees on topics such a cybersecurity and data privacy, funding challenges, public safety, securities litigation, and new member education. NAPPA also publishes a semi-annual newsletter, The NAPPA Report, that allows members to provide articles relevant for their peers in the public pension world.

I began my involvement as a member while working as Special Counsel for Ethics in the Office of the New York State Comptroller in the mid-2000s. After joining Cohen Milstein in 2011, I became involved with the section on Fiduciary and Plan Governance, presenting and organizing programs, and then was asked to assist with the New Member Education Committee. In 2024, I was thrilled when then-NAPPA President Laura Gilson, the General Counsel of the Arkansas Public Employees Retirement System, asked me to serve as Vice President. I’ve been lucky to see NAPPA from the perspectives of both in-house and outside counsel to public pension plans, which I think enhances my capacity to have a positive impact as President.

What really distinguishes NAPPA members is their commitment to the mission. Protecting the retirement security of educators, public safety officers, and other government employees is critically important, especially at a time when it feels as though government employees are under attack. It’s meaningful work for these attorneys, whose efforts benefit millions of retirees and the beneficiaries who depend on public pensions. Indeed, I’m a member of a public pension system after 20 years of public service in New York State, so I fully appreciate how important that pension check is to the beneficiaries of our clients. It’s essential to ensure that those checks get to those who devoted their careers to public service. We’re all proud to play a role in that important work.

LB: I know what you mean: I get one of those checks every month and share your enthusiasm and commitment to the beneficiaries of the public pension systems. To keep up to date with your practice, you recently attended NAPPA’s annual summer conference, which is where you became President. What were the most salient issues on the agenda?

SMD: There are some issues that are perennial, so NAPPA covers them at each meeting–professional ethics, recent litigation, federal legislation, and tax changes, for example. Other topics are more, well, topical—dependent on current trends. For example, cybersecurity and data privacy is top of mind these days, and we had a panel on that topic. I moderated a panel discussing the challenges of public comment periods on Board meeting agendas, and how to craft written policies that satisfy the First Amendment while allowing boards to function efficiently and effectively. We had a very well-received panel with Julie Reiser, co-chair of the firm’s securities practice, discussing the implications for public pension plans wrought

by the U.S. Supreme Court’s decision to overturn the Chevron deference doctrine. It was a wide-ranging agenda designed to keep public pension attorneys well informed.

LB: How does your work, and now leadership, at NAPPA complement your practice?

SMD: The best part is getting to know lawyers from around the country doing public pension law. I have learned so much from these people over the years. Of course, as I’ve gotten to know them, I feel comfortable calling them to ask questions, finding out how they approach challenges, learning what is new and coming my way. And I do like to help other attorneys, especially the new generation of lawyers who will be representing public pension systems for decades to come; the trust funds at the heart of the public pension world are not just long-term investors but are essentially perpetual ones, so it is not that hard to imagine that some of these lawyers new to NAPPA will be leaders of NAPPA in 2050. I enjoy that aspect of the organization and I hope that will be a part of the membership initiative I can foster as President.

LB: Thanks, Suzanne, for sharing more about NAPPA. Good luck in leading the organization.

On August 28, 2025, the U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN) issued an Advisory and Financial Trend Analysis on Chinese money laundering networks (CMLNs).

Chinese money laundering networks pose a significant threat to the U.S. financial system. FinCEN’s Financial Trend Analysis highlights the scope and breadth of CMLN activity in the United States. FinCEN analyzed 137,153 Bank Secrecy Act (BSA) required Suspicious Activity Reports filed by financial institutions between January 2020 and December 2024 that described suspected CMLN-related activity, totaling approximately $312 billion in suspicious transactions.

Below are highlights from the reports:

What are CMLNs?

- CMLNs are professional money laundering networks that are based in the People’s Republic of China (PRC), the United States, or other parts of the world. As discussed in the Advisory, CMLNs are often used by Mexico-based cartels to launder drug proceeds into the U.S.

- CMLNs often recruit private individuals who carry passports from the PRC to play a role, wittingly or unwittingly, in these networks to launder money across the globe.

- Chinese citizens’ demand for large quantities of U.S. dollars and cartels’ need to launder illicit U.S. dollar proceeds has resulted in a mutualistic relationship wherein cartels sell off illicitly obtained U.S. dollars to CMLNs who, in turn, sell the U.S. dollars to Chinese citizens seeking to evade China’s currency control laws.

CMLNs May Recruit Employees Inside Financial Institutions.

- CMLNs often utilize trade-based money laundering, money mules, and online mirror transaction methodologies involving fake trading platforms.

- CMLNs may recruit financial institution employees to act as insiders or infiltrate and place CMLN members within a financial institution to assist in money laundering schemes.

- CMLNs may also provide money mules with counterfeit Chinese passports to facilitate account opening and other illicit financial behavior.

CMLNs Favor Real Estate Purchases for Money Laundering.

- As discussed in the Financial Trend Analysis, financial institutions filed 17,389 SARs between 2020 and 2024 associated with more than $53.7 billion in suspicious activity involving the real estate sector.

- CMLNs may use money mules, like Chinese investors, or shell companies to purchase U.S. real estate with laundered funds.

Please read FinCEN’s full Advisory and Financial Trend Analysis for a comprehensive list of red flag indicators.

++++++++++

FinCEN requires financial institutions to file a SAR if it knows, suspects, or has reason to suspect a transaction conducted or attempted by, at, or through the financial institution involves funds derived from illegal activity. A SAR can be accessed through the Bank Secrecy Act (BSA) E-Filing System.

If you believe you have witnessed a suspicious activity involving money laundering, we encourage you to contact a Whistleblower lawyer, who focuses on FinCEN-related matters.

About the Author

Christina McGlosson, special counsel in Cohen Milstein’s Whistleblower practice, focuses exclusively on Dodd-Frank Whistleblower representation. She is the former director of the Whistleblower Office in the Division of Enforcement at the U.S. Commodity Futures Trading Commission. She was also a senior attorney in the SEC’s Division of Enforcement, where she assisted in drafting the SEC rules to implement the whistleblower provisions of Dodd-Frank. She also served as Senior Counsel to the SEC’s Director of the Division of Enforcement, and Senior Counsel to the SEC’s Chief Economist.

Christina represents whistleblowers in the presentation and prosecution of fraud claims before the SEC, CFTC, FinCEN-, as part of the U.S. Treasury, the Department of Justice, and other federal government agencies.

Christina McGlosson, Special Counsel: Dodd-Frank Whistleblower Practice

Cohen Milstein Sellers & Toll PLLC

1100 New York Avenue, NW

Washington, DC 20005

E: cmcglosson@cohenmilstein.com

T. 202-988-3970

Advertising Material. This content is informational in nature and should not be read or interpreted as legal advice. Should you need legal advice, please contact a lawyer.

Expert Analysis by Rebecca Ojserkis

After decades of standard practice, the U.S. Court of Appeals for the Fifth Circuit and the U.S. Court of Appeals for the Sixth Circuit each adopted their own new stricter standards to issue notice to collective action opt-in plaintiffs in Swales v. KLLM Transport Services LLC in 2021,[1] and in Clark v. A&L Home Care and Training Center LLC in 2023.[2]

Over the past four years, defendants in other circuits have pushed, without success, for the expansion of these more stringent procedures. As recently as July, the U.S. Court of Appeals for the Ninth Circuit rebuffed such efforts.[3]

But the U.S. Court of Appeals for the Seventh Circuit has now charted an altogether new ground. On Aug. 5, the court issued a ruling in Richards v. Eli Lilly & Co., in which it announced a new approach for district courts to determine whether to issue notice to opt-in plaintiffs.[4]

The contours of the test will only fully take shape as district courts in the Seventh Circuit tackle implementing this new standard.

Notice and Why It Matters

Legislation including the Fair Labor Standards Act, the Age Discrimination in Employment Act and the Equal Pay Act allow workers to litigate their claims together in collective actions.

Specifically, the statutes authorize plaintiffs to bring suit on behalf of “themselves and other employees similarly situated.”[5]

Less than 10 years after its passage, Congress amended the FLSA — in response to the proliferation of union‑initiated suits — to require each similarly situated worker to file a written consent to join the suit.[6]

The statute of limitations on the claims of each worker is not tolled until the court receives their personal consent.[7]

The need to affirmatively opt in distinguishes collective actions from class actions, where all but the named parties can remain absent. The intent of this approach was to create assurances that the workers wanted to be bound by any judgment.[8]

However, in order to submit a written acknowledgment that they want to be part of a representative action — and stop the clock on their claims expiring — workers must know about the action. That is where the question of notice comes in.

Existing Standards to Issue Notice

In 1989, the U.S. Supreme Court confirmed in Hoffmann-La Roche Inc. v. Sperling that trial courts must inevitably get involved in the notice process.[9] While encouraging early intervention, the high court reserved for district judges’ discretion the details of how they would exercise their role.[10]

Since then, the majority of district courts have followed a variation of the Lusardi two-step test, derived from the U.S. District Court for the District of New Jersey’s 1987 decision in Lusardi v. Xerox Corp.[11]

Under this approach, courts have issued notice to putative members of the collective early on in the litigation, after only a modest showing that they are similarly situated to the named plaintiffs.

In the past four years, however, the Fifth and Sixth Circuits have erected two new, but different, thresholds to issue notice. The Swales and Clark tests require substantial discovery, and thus time, to meet in order to show that workers are similarly situated by, respectively, a preponderance of the evidence or a strong likelihood.[12]

Earlier this summer in Harrington v. Cracker Barrel Old Country Store Inc., the Ninth Circuit refused to jump on either bandwagon and reiterated its commitment to its two-step precedent.[13]

In 2020, the Seventh Circuit punted on how and when courts should issue notice to opt-in plaintiffs in Bigger v. Facebook Inc.[14] But it has now weighed in.

The Seventh Circuit’s New Guidelines

The underlying suit that led to the Seventh Circuit’s new standard, Richards v. Eli Lilly & Co., involves Age Discrimination in Employment Act claims alleging that the pharmaceutical company overlooked employees who were over the age of 40 in its promotion practices.[15]

The Seventh Circuit accepted an interlocutory appeal from the U.S. District Court for the Southern District of Indiana and agreed to provide “clearer guidance” to lower courts on the necessary showing for court-issued notice.[16]

The circuit’s holding, intending to provide a “uniform, workable framework,” outlines a multipart decision tree.[17]

First, plaintiffs must present evidence that there is at least a dispute of material fact as to whether the named and opt-in plaintiffs are similarly situated, i.e., subject to a common policy or practice.[18]

Like Lusardi step one, evidence can come in the form of affidavits and counter‑affidavits.[19] Defendants may put forth rebuttal evidence to which the plaintiffs may then respond.[20]

After a fact dispute is identified, the district court can choose to issue notice, with a decision on certification to come after the completion of the opt-in process and discovery.[21]

Alternatively, the district court can authorize tailored discovery and still require a certification decision prior to notice.[22] Prenotice discovery could be limited to only part of the similarly situated analysis, or it could be more encompassing and overlap with merits issues.[23]

In short, unlike the existing three tests, the Richards standard presents district courts with flexible options on how to proceed.

In setting this new standard and rejecting the three existing ones, the Seventh Circuit invoked three principles that it drew from Hoffmann-La Roche.[24] They are the importance of timely and accurate notice, judicial neutrality, and the use of court discretion to prevent abuses and ensure efficient and proper joinder.[25]

The Implications of Richards

The Seventh Circuit stated that it set out to clarify how district courts should be “assessing the propriety of notice to a proposed collective.”[26] Yet its road map leaves many unanswered questions for district courts to grapple with.

For instance, take the open questions around prenotice discovery. The decision does not restrict the types of discovery authorized. Will document productions require e-discovery? Will depositions take place? If, for example, depositions of a corporate representative or a named plaintiff occur, and the questioning is tailored to the similarly situated topic, can these parties be deposed on other merits issues in a second sitting?[27]

Relatedly, the court does not specify how long the discovery and briefing on certification should take, except to discourage unnecessary delay.[28] What does this process of unknown length mean for workers’ running statute of limitations? The Seventh Circuit encourages, but does not require, equitable tolling during this period.[29]

In Clark, two judges on the Sixth Circuit panel gave a similar nudge to district courts,[30] which took the hint and now regularly equitably toll opt-in plaintiffs’ claims.[31] Will district courts in the Seventh Circuit take a similar tack?

Likewise, in Richards, the Seventh Circuit offered that a district court could dismiss a motion for notice without prejudice, subject to reconsideration with later acquired evidence.[32] Will courts embrace this invited flexibility?

Practically, it remains anyone’s guess how this new standard will play out. Will courts’ implementation of Richards operate more like the later notice of Swales and Clark, or will it bear more resemblance to Lusardi? Will employers still stipulate, as some did, to sending early notice? If so, will courts allow, and abide by, such agreement?

Finally, the panel did not speak in unison with respect to which party has the burden of moving for certification or what the burden of persuasion is.

The opinion was authored by U.S. Circuit Judge Thomas Kirsch and joined in full by U.S. Circuit Judge John Lee, who said in passing that they “presume that plaintiffs must establish their similarity at the certification stage by a preponderance of the evidence.”[33]

But in a separate concurrence, U.S. Circuit Judge David Hamilton criticized this discussion as substantively incorrect and beyond the scope of the question presented.[34] So, will district courts take the majority’s language as binding authority or merely influential dicta?

In the months and years to come, parties and district courts will wrestle with these and more questions about how to implement this notice standard in collective actions. But they should not anticipate further guidance from the Seventh Circuit, as it warned that it will not involve itself in a slew of interlocutory appeals to hash out every detail.[35]

The Supreme Court, however, may have more to say. Following the Ninth Circuit’s two-step embrace, Cracker Barrel has sought and received a stay of the Harrington decision while it petitions for writ of certiorari. The Seventh Circuit granted Eli Lilly’s motion seeking the same.[36]

Conclusion

Workers and employers should keep a close watch on whether this now four-way circuit split attracts the highest level of review.

In the meantime, workers and employers should embrace that the question of notice will be tailored to the nuanced facts of each case in the Seventh Circuit. Depending on what makes plaintiffs similarly situated from case to case, they may need to prepare for early discovery or an early opt-in process.

One-size-fits-all is no longer the norm within the Seventh Circuit.

Cohen Milstein’s nationally recognized antitrust practice group recently secured a $375 million antitrust settlement benefiting more than a thousand mixed martial arts fighters who had accused promoter Ultimate Fighting Championship (UFC) of unlawfully achieving market dominance that locked them into unfair, low-paying contracts.

U.S. District Judge Richard F. Boulware granted final approval to the deal on February 6, 2025, six months after saying he wanted a deal that would return “life changing” money to the Plaintiffs. Litigated over more than a decade, the antitrust class action showcases Cohen Milstein’s ability to achieve justice for its clients by outmaneuvering and outlasting deep-pocketed corporate defendants.

The settlement in Le, et al. v. Zuffa LLC (dba UFC), et al., 15-cv[1]01045-RFB-BNW (D. Nev.), covers more than 1,100 fighters who competed in UFC-promoted MMA bouts taking place or broadcast in the United States from December 16, 2010 to June 30, 2017.

Comparing their victory to “the end of a very, very long fight count,” Nate Quarry, one of the six original Le plaintiffs, told an interviewer that he and other plaintiffs broke into applause when the judge announced his approval. “Knowing that we get to split hundreds of millions of dollars between over eleven hundred fighters, that is an amazing feeling,” he said.

Under the settlement, Plaintiffs’ attorneys said 35 fighters should receive more than $1 million, about 100 fighters will get more than $500,000, and most of the remaining fighters in the class will be allocated amounts of between approximately $50,000 and $250,000. According to the Plan of Allocation, the minimum individual recovery is $15,000.

Fighters who have participated in UFC bouts since July 1, 2017 continue to litigate a second antitrust class action, Kajan Johnson, et al. v. Zuffa, LLC, which was filed in 2021 by Cohen Milstein and its fellow co-lead counsel.

Quarry, who has been vocal about the physical and financial toll caused by his championship MMA fighting career, said he and other Plaintiffs will continue the legal fight until the rules are changed for current and future MMA fighters. “… [O]ur goal from the very beginning was to hopefully get some monetary relief for the fighters that had been just horribly shortchanged. But then also we wanted to change the sport,” he said.

In certifying the Le class in 2023, Judge Boulware said plaintiffs had established that UFC parent company Zuffa had “willfully engaged in anticompetitive conduct to maintain or increase their market power.”

“Due to this anticompetitive, coercive conduct, fighters were trapped by Zuffa’s exclusionary contracts and their restrictive terms, creating a situation in which Zuffa had unfettered power and opportunity to suppress fighters’ compensation,” the judge wrote..

Dating from at least 2010, Plaintiffs alleged that UFC’s anticompetitive behavior allowed it to retain more than 80% of all revenue generated by MMA events in the U.S., while paying UFC fighters a fraction of what they would earn in a competitive marketplace. That percentage remained unchanged despite the explosive growth of Zuffa, which promoter Dana White and brothers Lorenzo and Frank Fertitta purchased for $2 million in 2001 and sold 15 years later for roughly $4 billion.

According to Judge Boulware, Plaintiffs established that UFC achieved its market power through anticompetitive means like buying and shutting down rival companies and “locking up” fighters into unfavorable and exclusionary three- or four-bout contracts. Fighters had no ability to negotiate terms, since UFC was effectively their only potential employer. And while UFC could drop fighters without explanation, the contracts barred the fighters from going elsewhere.

Moreover, UFC strong-armed fighters into signing new contracts before the old ones expired through its power to match them with unfavorable opponents in their remaining bouts, making the contracts “effectively perpetual,” the judge said.

As Nate Quarry put it in a 2024 interview: “They just get blacklisted, they get cut. They get put on the undercard. They are given opponents that aren’t going to be a good match up for them … The UFC is very vindictive. You’re either with the company or you’re against it.”

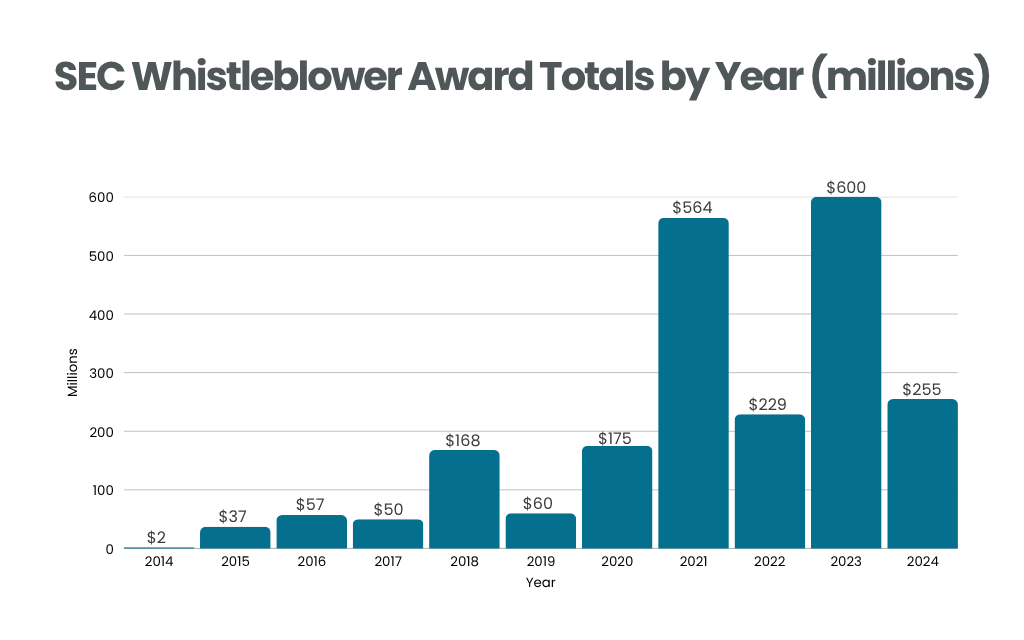

Even the largest and longest-running frauds can be brought to a screeching halt by a single person who uncovers the scheme and reports it to the government. In recognition of the critical role played by whistleblowers, a number of programs have been established to provide them with substantial financial awards if their information leads the government to recover money from the wrongdoers.

One example is the Securities and Exchange Commission Whistleblower Program. It was established after the Financial Crisis of 2008 and incentivizes whistleblowers to come forward by offering financial awards generally equal to 10-30% of the amounts that the SEC recovers based on the whistleblower’s information. These awards can be substantial. As shown in the graph below, there has been a broad upswing in the amounts of awards paid to whistleblowers by the SEC, punctuated by some extraordinary years that included particularly large awards.

Three Things to Know About the SEC Whistleblower Program

- The identity of whistleblowers is treated as confidential by the SEC. The SEC will take all reasonable steps to preserve whistleblower confidentiality and does not disclose publicly the identity of whistleblowers even at the end of a case when an award is made. In fact, whistleblowers who are represented by counsel are allowed to submit their information to the SEC without revealing their identity even to the SEC, unless and until the whistleblower applies for an award.

- There are many procedural rules that whistleblowers must follow in order to be eligible for an award, including rules about who can be a whistleblower, when their information must be reported, in what form, and the types of information that qualify for an award. There are also rules that concern how whistleblowers can make an application for an award if a recovery is obtained by the SEC, and the factors that will be considered in determining the amount of an award.

- While a whistleblower must provide information to the SEC that it is not already aware of to qualify for an award, there is no requirement that a whistleblower be a corporate insider. Indeed, many successful SEC whistleblowers are not insiders – they may be industry professionals who came upon evidence of fraud or other securities law violations in the course of their work, or who investigated a company and discovered those violations.

Navigating the Whistleblower Process: Don’t Go It Alone

Individuals who have information about fraud and who wish to participate in a whistleblower award program should retain experienced whistleblower counsel to advise them throughout the process on how to:

- Gather the supporting evidence

- Submit their information to the government in a comprehensive and persuasive manner

- Comply with all procedural requirements to be entitled to an award

- Work productively with the government to assist and facilitate their investigation and enforcement efforts

- Apply for and obtain the highest possible award if the government obtains a recovery

Make Your Information Count

The decision to blow the whistle can be one of the most impactful actions an individual can take to expose fraud, protect investors, and uphold the integrity of our markets. The SEC Whistleblower Program and others like it offer meaningful awards for those who come forward with original, credible information.

If you believe you’ve uncovered fraud, your next step matters. The path to a successful whistleblower award is complex, but you don’t have to navigate it alone. Our team has the experience to help you build a powerful submission, safeguard your interests, and pursue the award you deserve.

Remember, one person can put a stop to fraud.

A federal judge in Colorado has granted preliminary approval of a $27 million settlement in a securities lawsuit brought against InnovAge Holding Corp. by Cohen Milstein on behalf of its clients the El Paso Firemen & Policemen’s Pension Fund, the San Antonio Fire & Police Pension Fund, and the Indiana Public Retirement System.

The settlement would end three years of hard-fought litigation against multiple defendants: InnovAge, a healthcare provider specializing in senior care; certain of its former executives; private equity firms— Apax Partners and Welsh, Carson, Anderson & Stowe—who owned controlling stakes in InnovAge; and underwriters of InnovAge’s initial public offering.

Lead Plaintiffs alleged that Defendants made false and misleading statements regarding InnovAge’s regulatory compliance, the quality of its care model, and the viability of its growth strategy. Government audits uncovered significant compliance violations, including woefully understaffed care centers. The sanctions that followed, including an enrollment freeze, hindered InnovAge’s ability to grow and caused the stock price to plummet, according to Lead Plaintiffs’ complaint.

“When private equity pushes for profits in the healthcare space, it raises risks for patients and shareholders alike,” said Molly Bowen, a partner on Cohen Milstein’s InnovAge team. “By fighting for and obtaining this excellent result, our clients showed how engaged pension funds can hold public companies accountable for fraud and benefit their fellow investors.”

The three Lead Plaintiffs and Lead Counsel Cohen Milstein conducted extensive discovery and motions practice that provided ample evidence about the strengths and risks of the case. Lead Plaintiffs investigated, drafted, and filed a detailed amended complaint and defeated, in large part, Defendants’ repeated motions to dismiss. They engaged in substantial fact discovery, including exchange of document requests and interrogatories, production of hundreds of thousands of pages of documents, serving subpoenas on third parties, and conducting Rule 30(b)(6) depositions of the Lead Plaintiffs and their three investment managers—a total of eight individuals representing six different entities. Lead Plaintiffs also successfully moved for class certification, supported by an expert report on market efficiency and damages.

The $27 million settlement is a class-wide recovery that exceeds the typical recovery in securities class actions, particularly for a case where most damages stem from claims arising under a company’s statements in connection with an initial public offering.

The result is even more remarkable considering the particular challenges presented by InnovAge’s precarious financial state. In virtually all cases, extending litigation for years—through additional dispositive motions, trial, and appeals—carries a risk that the class might recover less (or even nothing). Here, InnovAge’s limited insurance and a significant decline in its stock price during the litigation heightened that risk. During the litigation, InnovAge’s stock price fell from around $6.50 per share to as low as $2.75 per share, raising a risk that the company would have difficulty funding a settlement.

On June 17, 2025, US District Judge William J. Martinez granted preliminary approval of the settlement in the case, which is captioned El Paso Firemen & Policemen’s Pension Fund v. InnovAge Holding Corp. (21-cv-02270-WJM-SBP (D. Colo.).

In the coming months, Cohen Milstein will work with the court-approved claims administrator to oversee the process of disseminating notice of the settlement. Impacted investors can find more information at https://www.strategicclaims.net/innovage/. Judge Martinez scheduled a final approval hearing for November 26, 2025.

By Rebecca Ojserkis

While the Fair Labor Standards Act inches closer to its 90th birthday, its statutory text has attracted significant judicial attention in recent years on foundational legal questions.

In particular, two circuit splits have been bubbling on the proper standard to issue notice and the scope of personal jurisdiction requirements.

On July 1, the U.S. Court of Appeals for the Ninth Circuit weighed in with its ruling in Harrington v. Cracker Barrel Old Country Store Inc. — adding another decision to the increasingly lopsided scales. In short, the two-step certification process continues to reign supreme.

However, plaintiffs are increasingly stymied in bringing nationwide collective actions anywhere except where employers are headquartered or principally based.

With cases pending in other jurisdictions, the scales may continue to tilt or regain balance in the coming months.

Two-Stepping Remains in Fashion

Although the FLSA invites workers to collectively vindicate their rights under the statute, its text does not specify how courts should determine whether workers are sufficiently similarly situated to proceed as a group.

Historically, many appellate and trial courts, in their discretion, have adopted a two-step process that is often credited to the 1987 decision in Lusardi v. Xerox Corp. in the U.S. District Court for the District of New Jersey.

The first step merely asks whether the court should authorize notice to putative collective members. Thus, courts expect only a modest showing of connective tissue between the proposed collective — prior to, or following, only limited discovery.

Later, at step two, courts apply a more stringent benchmark when revisiting their earlier determinations as to whether the plaintiffs are sufficiently similarly situated, such that the cases can proceed en masse.

This widely employed procedure began to come under fire, though, as the U.S. Court of Appeals for the Fifth Circuit, and then the U.S. Court of Appeals for the Sixth Circuit, adopted heightened bars to collective certification in 2021 and 2023, respectively.

In subsequent years, employers have regularly forecast a sea change when pressing for other jurisdictions to follow their sister circuits. But the promised sweep of the Fifth and Sixth Circuit’s new notice standard has not come to pass.

Except for a handful of outlier decisions, most district courts have stayed the two-step course. This majority has included courts in the Ninth Circuit, which approved of two-step use in Campbell v. City of Los Angeles in 2018.

The Ninth Circuit’s Ruling

With its July 1 wage and hour ruling in Harrington v. Cracker Barrel, the Ninth Circuit has reiterated its embrace of the two-step procedural mechanism.

The case involved a challenge by current and former Cracker Barrel employees for wage and hour law violations related to tipped workers. The court declined the defendant’s request to adopt a heightened standard for issuing notice, on the ground that the Ninth Circuit had already decided this issue in Campbell.

The court’s brief analysis has relegated to a footnote what had been the subject of commentator forecasting: that the U.S. Supreme Court’s FLSA ruling this year may signal a turning of the tide toward the collapse of the notice and collective certification rulings.

On Jan. 15, in EMD Sales Inc. v. Carrera, the Supreme Court held that the preponderance of the evidence, the default standard of proof, governs whether a particular FLSA exemption applies.

But in its Harrington decision, the Ninth Circuit easily dispatched with the defendant’s analogy since the high court had “said nothing about how a district court should manage a collective action or the procedure it should follow when determining whether to exercise its discretion to facilitate notice to prospective opt-in plaintiffs.”

Even on the next question presented — whether notice could issue when fact disputes remained about the arbitrability of claims — the court in Harrington emphasized how notice dissemination falls under the district court’s discretion over case management.

The panel did not note, but could have, that courts have always had to satisfy themselves at the step two certification stage that FLSA plaintiffs were similarly situated by a preponderance of the evidence.

While a possible change still threatens pending appeals[15] and the parties’ petitions for rehearing, the Harrington court’s succinct and unanimous handling of this question suggests that early FLSA notice — all that is at issue at step one of the two-step certification process — may remain the norm.

Barriers Mount for Nationwide Collectives

Mirroring trends with respect to other nationwide procedural vehicles, federal courts of appeal have increasingly taken issue with multistate FLSA collectives, depending on where they are filed.

In 2017, the Supreme Court issued a seminal personal jurisdiction ruling in Bristol-Myers Squibb Co. v. Superior Court of California, a consolidated mass action involving state law claims. The court held that each plaintiff needed to, but did not, establish specific personal jurisdiction over the out‑of-state defendant corporation.

Employers have argued — mostly with success — that Bristol-Myers should also apply to federal courts’ jurisdiction over FLSA claims.

Until the Harrington decision, the circuits had split four to one, with the majority of circuits — at times over vigorous dissents — expanding Bristol-Myers to hold that each FLSA opt-in plaintiff must establish personal jurisdiction as to each defendant.

The Ninth Circuit joined a growing chorus with its decision in Harrington, vacating and remanding the case to the U.S. District Court for the District of Arizona to reassess its issuance of notice beyond plaintiffs who worked in Arizona, the state where the suit was brought. Other circuits are expected to take a stand soon.

Functionally, these decisions render collective actions impossible for conduct occurring in several states, unless the suit is brought in employers’ backyards — where general jurisdiction exists.

This line of authority results in what is effectively corporate forum shopping, because plaintiffs must file nationwide FLSA collective actions in the states that their employers choose to call home.

While some may view this as a mere inconvenience, this procedural hurdle can pose, at best, inefficiencies for the parties and courts, and at worst, a substantive bar to the vindication of workers’ rights.

Take, for example, a minimum wage challenge that is brought against two joint employers, each with their own corporate home. Under the decisions of the Ninth Circuit and others, plaintiffs must file separate, parallel actions — that is, if they can find counsel with the resources to litigate on a dual track.

Practically speaking, the harder it is for workers to bring collective challenges, the greater the risk that employers might violate wage and hour laws, including tip compliance provisions, on local and larger scales.

However, there may be a silver lining for workers. While the Ninth Circuit gave the notice questions the back of the hand, it delved more deeply into the topic of personal jurisdiction.

Among the reasons for its ruling, Harrington emphasized the contrast between class and collective actions. The Ninth Circuit’s predecessor sister circuits did the same, grounding their conclusions on the different rigors to which classes and collectives are subject.

By extension of the logic in the four aforementioned opinions, the standard for finding that plaintiffs are similarly situated for collective certification should be decidedly more lenient than the test for class certification under Rule 23 of the Federal Rules of Civil Procedure, which demands meeting several explicit and implied requirements across the rule’s subsections in order for parties to demonstrate the need to proceed collectively.

These judicial rulings, of course, need not be the final word. There is also a role for legislatures to play in changing this landscape. To start, Congress could amend the FLSA to provide for nationwide service of process, which would alter courts’ specific jurisdiction analysis to focus on defendant companies’ contacts with the U.S. as a whole.

Alternatively, states could expand the realm of general jurisdiction by mandating implicit consent to the state’s exercise of personal jurisdiction as a cost of registering to conduct business.

In sum, while the Ninth Circuit’s decision in Harrington v. Cracker Barrel does not break new ground, it suggests a settling of two procedural trends in FLSA jurisprudence — when to issue notice and where nationwide collectives can be filed — rather than deepening circuit splits.

For this edition of the Fiduciary Focus column, I was thrilled to sit down with Andrew Roth, who became the Executive Director and CEO of the Colorado Public Employees’ Retirement Association (PERA) in May of 2024.

Andrew has deep experience in public pensions, having arrived in Denver from Austin, where he was the Deputy Director of the Teacher Retirement System of Texas (TRS). Prior to that, he served as the Benefits and Services Executive Officer at the California State Teachers’ Retirement System (CalSTRS). Further evidencing his leadership role in the world of institutional investors, Andrew was recently elected to the Board of Directors of the Council of Institutional Investors (CII).

As you approach your first anniversary, how are you finding the transition to PERA, which is a bit smaller than TRS, but no less focused on the members and beneficiaries?

The transition from TRS to PERA has been greatly facilitated by a terrific executive team, supportive Board, and welcoming stakeholders. While PERA is a smaller organization than either CalSTRS or TRS in terms of assets under management and the number of both members and beneficiaries, what strikes me as unique is the complexity of the plan. Five divisions within the plan means five sets of distinct stakeholders, each with their own set of concerns. Complexity aside, PERA, like CalSTRS and TRS, is hyperfocused on its members, beneficiaries, and mission, which drives a strong collaborative culture that makes working here a rewarding experience.

What would you say are the biggest challenges you are facing in 2025 as you assist the PERA Board in fulfilling their fiduciary responsibilities?

The biggest challenge we’re facing in 2025 is the volatility in the market. PERA’s funded status is below the median of US Public Pension funds, which amplifies market uncertainties and swiftly captures the attention of the plan sponsor (the Colorado General Assembly) and our stakeholders. A big part of my job involves supporting PERA’s Board of Trustees with helpful information and guidance on complex investment, actuarial, and fiduciary concepts; when there’s a lot of noise generated by relatively short-term market events, that cacophony can distract and disrupt focus on PERA’s 30-year horizon and working toward the full funding of the plan.

Direction from Washington reflects very different approaches from those of the recent past, especially with changes in regulatory and economic priorities. How is PERA accommodating these adjustments in its planning?

Great question. PERA has historically, and continues to be, focused on generating the best risk-adjusted returns possible. We pay close attention to regulatory changes and economic priorities in both our state as well as in Washington. Shifts in priorities from either place result in the executive team and Board of Trustees making policy decisions as appropriate to accommodate the policy requirements generated either by our plan sponsor in the Colorado Legislature or by the federal government. PERA’s talented investment team’s focus on investing in what we know has served us well regardless of which direction the political winds blow.

There’s no doubt that the focus on ESG & DEI priorities has changed significantly in the current political climate. In what way should institutional investors focus on developments in this area?

A timely question, and one that is on the minds of many people in the financial world. After years of focusing on making improvements in the DEI-related space, new direction from the federal government raises significant questions and debate, and related activities may now result in serious consequences. Many corporate entities and institutional investors have responded by dropping or repurposing DEI-related initiatives to avoid triggering penalties or negative interest from the federal government. ESG is a little more complicated as due diligence requires investors to consider risk, including risks that may be related to environmental, social, or governance factors. Sound investment principles and fiduciary duties require institutional investors (and really any serious investor) to comprehensively consider all risks that may impact returns. Poor governance, unsound practices, and disregard for rules and regulations will negatively impact investment returns, which in my opinion means institutional investors will continue to evaluate risk and make decisions accordingly.

Artificial Intelligence (AI) is altering the way we think about accomplishing various tasks. Do you see this trend coming into play at PERA?

Yes, like most industries, public pension funds are considering AI technology and the use cases that can support and enhance our administration of the retirement plan benefits that are of crucial importance to our members and beneficiaries. While it undoubtedly has useful applications, AI requires scrutiny as its limitations and drawbacks are well documented and serious in nature. At PERA, we’ve established an AI policy and an AI council to evaluate the tools rapidly coming online in this space and assess how appropriate they are for our internal use. I’d describe PERA’s utilization of AI-related tools as somewhat limited in scope but useful in terms of facilitating production-related tasks.

You were recently elected to the Board of CII. How do you see this role as complimenting your role at PERA and assisting you in fulfilling your fiduciary duties?

As CEO, I am accountable for oversight of the entire organization, including the investment function. My previous roles in the public pension space were primarily focused on plan design, pension benefits, information technology, human resources, finance, shared services, and large-scale enterprise projects. Upon stepping into the CEO role at PERA, I wanted to lean in and deepen my investment knowledge. We are incredibly fortunate at PERA to have a talented and tenured investment team that has helped expedite this continued learning and development for me. Participating on the CII board provides me with an additional opportunity to expand my knowledge at an appropriate level about issues impacting institutional investors. This all helps me refine and calibrate the fiduciary lens through which I evaluate related issues affecting PERA and our important mission and purpose.

An Interview with Daniel S. Sommers by Kate Fitzgerald, Senior Manager, Marketing Communications

Daniel S. Sommers, a Cohen Milstein partner and former co-chair of the firm’s Securities Litigation & Investor Protection practice, is a highly regarded thought leader in securities class actions and investor rights. He is a member of the National Association of Public Pension Attorneys’ Securities Litigation Committee and former chair of the Council of Institutional Investors’ Markets Advisory Council, as well as a past chair of the District of Columbia Bar’s Investor Rights Committee of the Corporation for the Finance & Securities Law Section. His nearly 40 years of experience gives him special perspectives and having litigated securities class actions—both before and after the enactment of the Private Securities Litigation Reform Act of 1995 (“PSLRA”.)

Kate Fitzgerald: Tell us a little about the PSLRA and why it was enacted?

Daniel Sommers: The PSLRA had its genesis in the mid-1990s. It was drafted to address concerns about the utility and costs of securities class actions.

For example, there was a perception that securities class actions were generated by and for the benefit of plaintiffs’ lawyers, that plaintiffs were often retail investors with relatively small investment losses who had little incentive to supervise the litigation and often were “repeat” or “professional” plaintiffs, and that many cases were filed too quickly, were poorly investigated, or simply lacked merit.

There was also the perception that these cases imposed undue costs on issuers—especially the costs of discovery, which can be significant in securities class action cases.

In general, the intent of the PSLRA’s proponents was to enact legislation that would eliminate or at least reduce what they perceived to be “meritless” cases; to establish procedures to slow down the speed with which cases can be filed; to replace so-called “lawyer driven” litigation with litigation led by larger, sophisticated institutional investors that have the capability and incentive to supervise litigation due to their a large financial interest in the case; and to reduce the agency costs of these cases—especially those related to the discovery process.

KF: Who advocated for and against passing the PSLRA?

DS: The PSLRA was advocated for by business groups, such as the U.S. Chamber of Commerce and Business Roundtable, as well public companies, especially high-tech companies, which saw themselves as frequent targets at the time. In opposition to the PSLRA were plaintiffs’ lawyers, investor rights groups, and some academics who advocated for the importance of these cases to protect the rights of investors and argued that the proposed statute would preclude meritorious cases from proceeding.

Notably, this view was shared by President Clinton, who expressed his concerns about the proposed legislation and issued a veto. But that veto was overridden by Congress.

KF: Could you outline some of the more significant PSLRA provisions?

DS: Yes, the PSLRA contains many provisions that changed the way securities class actions were litigated. For example, the statute radically changed the process by which both the lead plaintiff and its counsel are appointed by the court.

Before the PSLRA, courts often gave control of cases to the investor that filed the initial case— regardless of the size of their investment or their loss, and regardless of the quality of their complaint or the capabilities of their counsel. In other cases, courts sometimes made judgments about which investor was best or had filed the best complaint or allowed various plaintiffs privately to agree on leading cases with groups of investors.

In response, the PSLRA created a very specific structure, methodology, and timeline that district courts must follow when appointing the lead plaintiff. This process remains unique to securities class action litigation.

For instance, the PSLRA directs courts to select as lead plaintiff the investor or group of investors with the greatest financial interest in the case, provided they also satisfy the class action adequacy and commonality requirements of Rule 23. This was a significant change from prior practice, where courts had significant discretion to appoint lead plaintiffs, and this change gave institutional investors a significant preference to be appointed as the lead plaintiff.

The PSLRA also established a 60-day window for investors to file lead plaintiff motions. This provision was intended to eliminate the race to the courthouse and to encourage sophisticated investors an opportunity to investigate the claims and to decide whether to lead these cases. Again, this was another mechanism that was intended to induce institutional investors to participate in these cases.

This was a significant change from prior practice where courts had significant discretion to appoint lead plaintiffs.

KF: That is a dramatic shift in procedure. How did the PSLRA impact discovery?

DS: The changes to the discovery process were also dramatic. The PSLRA imposed a mandatory stay of all formal discovery until defendants’ motion to dismiss is denied. There are very limited exceptions to the discovery stay.

Previously, district court judges had discretion to permit discovery to proceed while a motion to dismiss was pending and investors could use information learned in discovery to support the claims alleged in the complaint. The PSLRA almost entirely eliminated this option from investors’ arsenal. Now, investors and their counsel must marshal facts to support the claims in their complaint without any of the powerful discovery tools provided for by the Federal Rules of Civil Procedure.

KF: What else changed under the PSLRA?

DS: Another important change included in the PSLRA was the adoption of a heightened pleading standard that requires plaintiffs to plead their complaint with specific facts that give rise to a “strong inference” that each defendant acted with scienter—an intentional or reckless intent to deceive investors. This standard is to my knowledge higher than the standard in any other type of federal civil litigation and has resulted in investors’ counsel undertaking in-depth investigations to assemble very strong facts to support their claims. This change, along with the discovery stay provision, has presented a significant challenge to investors.

KF: And what about forward-looking statements?

DS: In general, the PSLRA immunized issuers from liability for forward looking types of statements, such as projections and forecasts about business plans or economic performance, if they were accompanied by “meaningful cautionary” language or if the information was “immaterial” to investors; or where the plaintiff fails to prove that the speaker made the statement with “actual knowledge” of its falsity.

KF: Any other material changes?

DS: Yes, there are several other important provisions. For instance, the PSLRA clarified that investors had the burden to prove that false statements made by defendants caused investor losses. It also created a 90-day lookback cap on recoverable damages to prevent a perceived windfall for investors in situations where a corrective disclosure causes a drop in the stock price, but the stock price rebounds in the 90 days following the class period.

The PSLRA also changed prior practice by limiting the instances when joint and several liability would be available to plaintiffs only to situations in which there is a finding that the defendant knowingly violated federal securities laws.

The PSLRA further required that courts make findings at the conclusion of a case as to whether any party or their counsel filed documents that contained baseless arguments and whether, as a result, sanctions are appropriate.

Finally, the statute set requirements for settlement notices, including disclosures about potential recoveries had the case gone to trial and attorneys’ fees.

KF: What has been the overall impact of the PSLRA on the role of institutional investors?

DS: As you can see, the PSLRA has dramatically changed the landscape of securities class action litigation—especially from the investor perspective. As to the success or failure of the statute, the results have been mixed, with some provisions being problematic for investors and others benefiting them.

Perhaps the greatest positive from the investor perspective has been caused by the lead plaintiff provision.

The PSLRA’s lead plaintiff process has unquestionably resulted in sophisticated investors, including institutional investors, becoming more engaged in securities class actions. These investors include public pension funds (including public safety funds), Taft-Hartley funds, and large, non-U.S. funds.

While most initial cases are still filed by retail investors, the PSLRA clearly achieved one of its goals, as it has led to a surge in institutional investor participation. One study indicates that between 1995 and 2002 institutional leadership in these cases increased from virtually zero to about 27% of all cases. And between 2010 and 2012 institutional investors were appointed lead plaintiff in 40% of all cases. Our own internal analysis of 2024 filings confirms this data.

KF: What have been the implications of this increased participation by institutional investors?

DS: There have been significant beneficial consequences of this trend. The data shows that the increased participation of institutional investors is associated with lower dismissal rates and larger recoveries for investors. In fact, institutional investors have served as lead plaintiffs in virtually all the largest securities class action recoveries post-PSLRA. By this measurement, the PSLRA did achieve one of its most important objectives – encouraging large, meritorious cases to proceed.

In addition, there is evidence that more sophisticated investors are better able to negotiate attorney fee caps, lowering attorney fees and increasing per share investor recoveries.

By these measurements, the PSLRA has achieved its objective to control costs and fees and increase net investor recoveries—all of which benefits investors

KF: What about the race to the courthouse issue?

DS: Eliminating the so-called “race to courthouse” has not been achieved. I think this is largely because the drafters of the PSLRA did not fully understand the dynamics of securities class actions. So, we still have a system where initial cases are filed shortly after the disclosure of an adverse event— typically by a small retail investor. However, the initial filing does trigger the 60-day lead plaintiff filing window for other investors, including institutional investors, to step forward, which as I mentioned is a benefit to all investors.

KF: What about the case quality issue?

DS: Anecdotally, I have observed over the last 30 years that the quality of work from plaintiff lawyers has generally improved. In particular, we see this reflected in the factual specificity in operative complaints, especially those filed by institutional investors. This is another important argument for institutional investors to serve as lead plaintiffs

KF: What about the impact of the automatic discovery stay?

DS: In terms of the automatic discovery stay provision, it met its stated objective: for plaintiffs, unfortunately, it has effectively thwarted their ability to obtain any formal discovery until resolution of the motion to dismiss.

Interestingly, however, it has encouraged plaintiffs’ counsel to sharpen their pre-filing investigation skills. So, we are seeing more robust pre-filing investigations, such as obtaining information from witnesses—including former employees of the issuer—and other important information that is used to bolster the complaint’s allegations. Unfortunately, the automatic discovery stay along with the statutory lead plaintiff process has increased the duration of these cases. For instance, the lead plaintiff process followed by the filing and litigation over an amended complaint can often take 6 months to a year before any formal discovery can proceed.

KF: Has there been a material drop in the number of filed cases?

DS: Simply put, no. There is no evidence that fewer cases have been filed post-PSLRA. On average around 225 securities class actions are filed per year, though obviously those numbers are higher in some years and lower in others.

KF: Are there any recent PSLRA changes or trends you anticipate?

DS: I see nothing on the horizon. After 30 years, the PSLRA is well established and deeply engrained in securities law jurisprudence. Indeed, most lawyers and judges have never experienced securities class action litigation without the PSLRA.

While both sides would still like to see material changes to the statute, there does not appear to be any public momentum for legislative change—although in our current political environment it is hard to predict what issues might take hold in Congress and elsewhere. 22 | cohenmilstein.com cohenmilstein.com | 23 So, it appears that the PSLRA, in its current form, is here to stay.

With that said, I anticipate that institutional investors will continue take on leadership positions— especially in cases involving serious allegations of misconduct and significant investor losses. From the investor protection point of view, this is certainly the most important and positive long-term consequence of the PSLRA.

For shareholders seeking to police corporate misconduct, the right to assert derivative claims— to sue on behalf of a corporation against officers, directors, and third parties whose actions have harmed the company—is a critical corporate governance tool.

Derivative litigation empowers shareholders to enforce compliance with fiduciary duties and ensure managerial accountability. A stockholder can assert such derivative claims either by filing a derivative complaint on the company’s behalf or by making a demand that the Board of Directors (Board) investigate and, if warranted, initiate a derivative action against the alleged wrongdoers. In either situation, the Board may appoint a Special Litigation Committee (SLC) which often becomes a central player in the investigation, any pending derivative litigation, and possible resolution of these claims.

To properly function, the SLC must be comprised of independent Board members. Once formed, the SLC should conduct a thorough investigation involving a review of internal documents, witness interviews, and consultations with independent counsel or experts, then produce a report of its findings and recommendations. The SLC’s ultimate recommendation may provide grounds for rejecting the claims, settling the action, or continuing to prosecute the lawsuit. If the SLC report recommends dismissal, shareholder plaintiffs have the right to obtain discovery as to the independence of the SLC and the basis for its findings.

Recently, Cohen Milstein has represented shareholder plaintiffs in several proceedings that illustrate the interplay between an SLC and a shareholder derivative litigation. In a pending stockholder derivative action involving Abbott Laboratories, plaintiffs allege a breach of fiduciary duties concerning the contamination of infant formula. An SLC appointed by Abbott’s Board to investigate plaintiffs’ claims moved to stay the case until it had finished its investigation. In partially denying the SLC’s motion, the Court held that plaintiffs were entitled to discovery of the same documents provided to the SLC to prepare its report. The Court noted that “[T]his discovery is necessary to prevent a special litigation committee from cherry-picking the facts highlighted in their report.” Armed with the discovery they obtain through the ruling, shareholders will have the right to challenge the SLC’s independence and conclusions if the SLC report seeks dismissal of the pending derivative litigation.

Similarly, Cohen Milstein recently filed a derivative action against officers and directors of Pegasystems Inc. related to a $2 billion judgment against the company for violating a competitor’s trade secrets. After several shareholders made demands on the company to investigate the board and management, it appointed an SLC, which rejected bringing claims against the alleged wrongdoers. In response, shareholders filed derivative litigation challenging the SLC’s report and independence.

In a different context, Cohen Milstein, on behalf of a shareholder client, recently sent a demand to a company’s board to investigate and commence derivative litigation against a third party who was culpable for participating with the company’s CFO in securities fraud. After an SLC investigation into potential claims, the board agreed to accept the demand and initiated litigation against the third party, which eventually settled for a substantial amount.

In sum, SLCs are a significant aspect of shareholder derivative litigation. They must be genuinely independent, procedurally thorough, and substantively fair. Shareholders, through the courts, must rigorously evaluate these attributes to ensure the integrity of the process and the protection of the corporation’s and shareholders’ interests.